Why a Tax Dollar Saved Today Is Worth More Than One Saved Tomorrow

The time value of money, in plain English

Most people think about taxes one year at a time: how much can I cut this year’s bill? That’s a good instinct, but it misses something important. A dollar of tax savings is not always worth a dollar. When you capture the savings matters just as much as how much you save, because money you keep today is worth more than the same money handed to you years from now.

This idea has a name — the time value of money — and it’s one of the most useful lenses for making smart tax decisions. Here’s how it works and why it should shape your planning.

The core idea: money now beats money later

Would you rather have $1,000 today or $1,000 five years from now? Almost everyone picks today — and they’re right to. The dollar you hold now can be invested, used to pay down debt, or put to work in your business. It starts earning immediately. A dollar promised in five years just sits in the future, doing nothing for you in the meantime, and inflation quietly eats away at what it will buy.

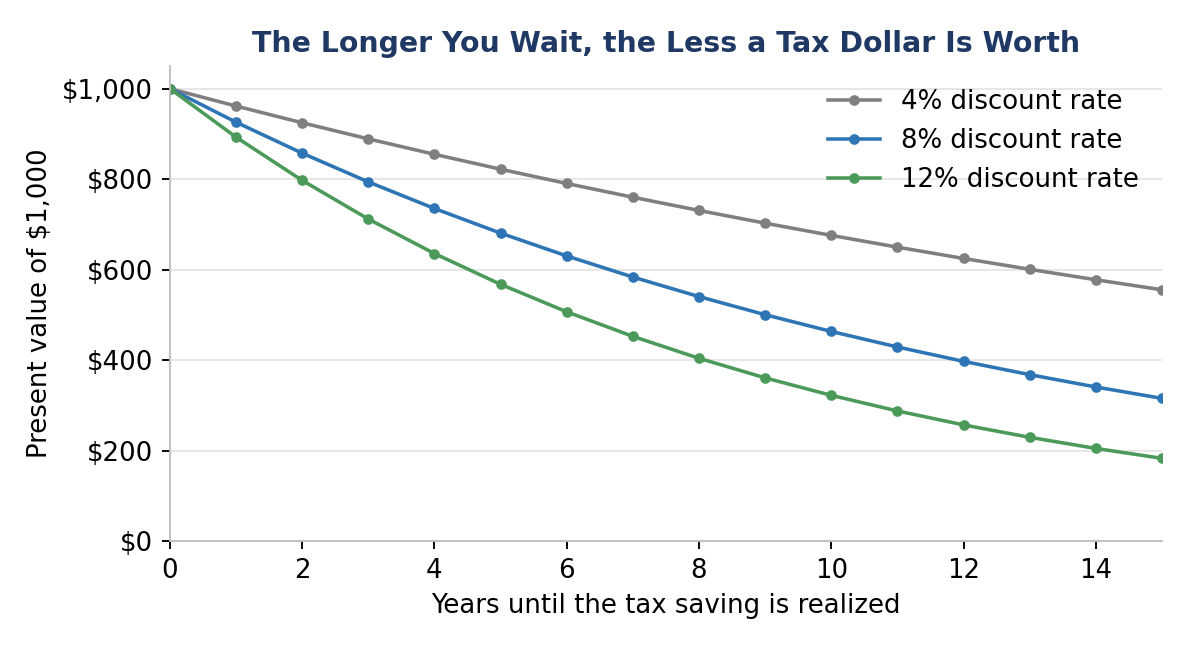

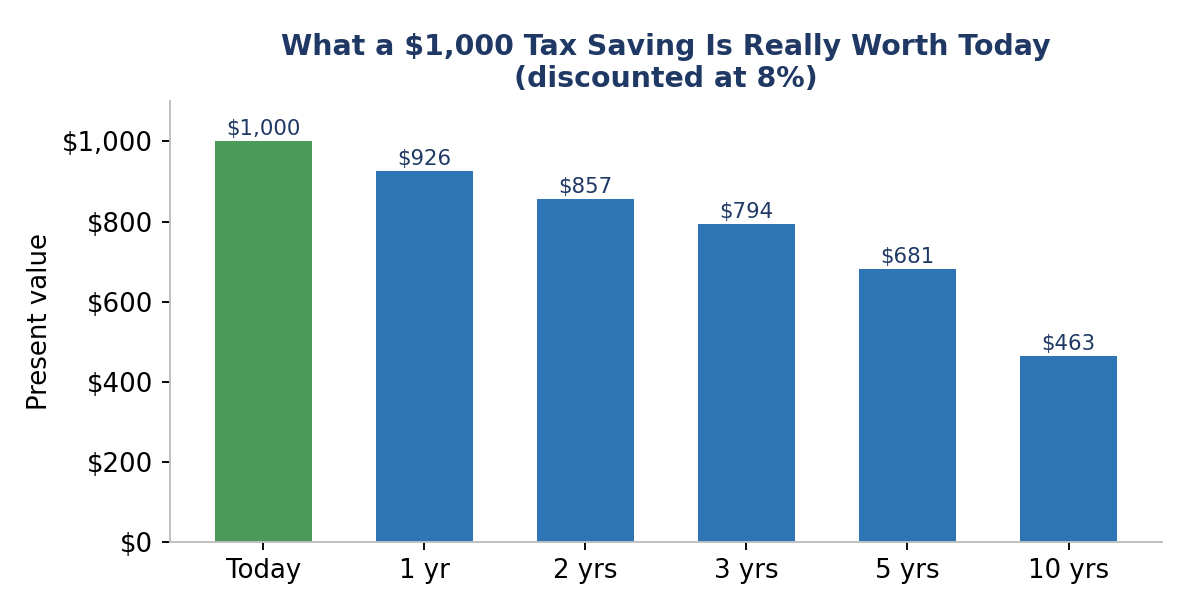

To compare money across time, we discount future dollars back to what they’re worth today. If you can earn 8% a year, then $1,000 arriving in five years is worth only about $681 in today’s money. The further out the dollar sits, the less it’s worth right now.

What this means for tax savings

Tax savings are just cash flows — money that stays in your pocket instead of going to the IRS. So the exact same logic applies. A deduction, credit, or deferral that puts money back in your hands this year is worth more than an identical one that pays off years down the road.

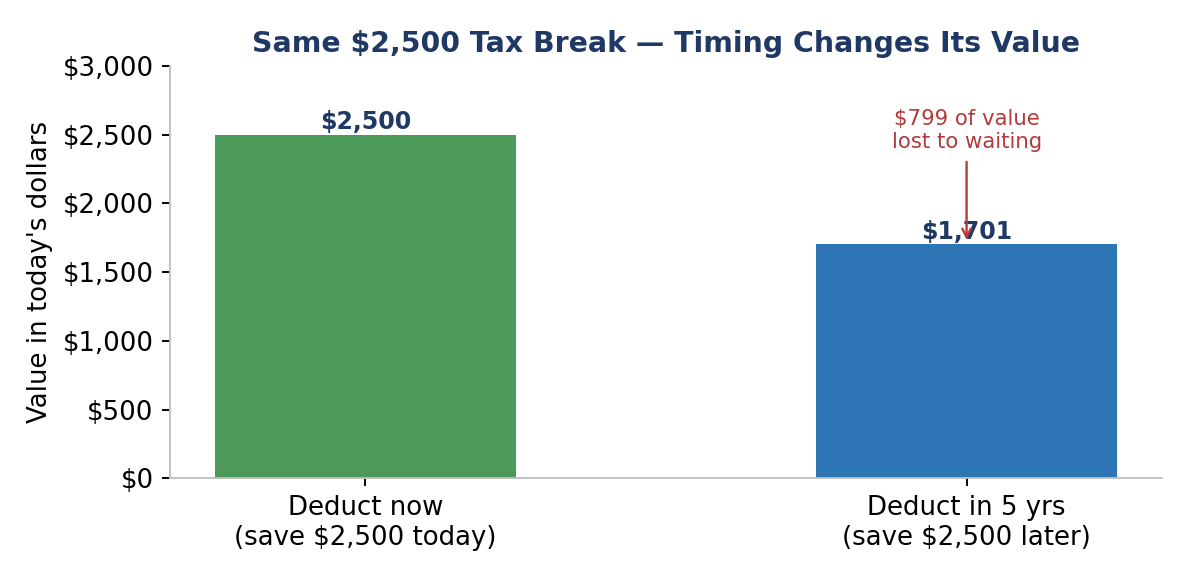

Say you’re in a 25% bracket and you have a $10,000 deductible expense. Claiming it saves you $2,500 in tax. Take that deduction now and the $2,500 is worth a full $2,500 today. Push the same deduction out five years and — even though it’s still $2,500 on paper — it’s really only worth about $1,701 in today’s dollars. Waiting quietly threw away roughly $800 of value.

The same saving, valued year by year

Here is how a $2,500 tax saving loses ground the longer it takes to arrive, using an 8% discount rate. Realized today, it is worth the full $2,500. In one year it is worth about $2,315; in three years about $1,985; in five years about $1,701; and in ten years just $1,158. The chart below shows how each year of delay chips away at what the saving is actually worth to you.

How to put this to work

The practical takeaway is simple: when you have a choice, lean toward capturing tax benefits sooner rather than later. Accelerating deductions into the current year, claiming credits as soon as you qualify, and deferring income where it makes sense all pull value forward in time — and pulled-forward value is worth more.

A few caveats keep this honest. If you expect to be in a much higher tax bracket next year, a deduction may be worth more then, and that larger benefit can outweigh the time-value cost of waiting. Cash-flow needs, changing tax law, and your personal rate of return all factor in too. The point isn’t that sooner is always better — it’s that timing has real, measurable value, and it deserves a seat at the table in every tax decision.

Bottom line: a tax dollar saved today is worth more than a tax dollar saved tomorrow. Treat the timing of your tax savings as seriously as the size of them, and you’ll consistently keep more of what you earn.

This article is for general educational purposes and isn’t individualized tax advice. Discount rates and tax brackets vary by situation — talk with your tax professional before acting.