What Are “Trump Accounts,” and How Do They Work?

If you have read our earlier note on why a tax dollar saved today is worth more than one saved tomorrow, the idea behind Trump Accounts will feel familiar. Time is the most powerful ingredient in any savings plan, and the newest account in the tax code is built entirely around giving a child the earliest possible start. Signed into law as part of the One Big Beautiful Bill Act and rolled out to families beginning in July 2026, a Trump Account is a tax-advantaged investment account opened for a child — seeded, in many cases, with $1,000 of government money.

The big idea

A Trump Account is essentially a retirement account that starts at birth. Money contributed on a child’s behalf is invested in a low-cost fund that tracks a broad U.S. stock index, and it grows on a tax-deferred basis — no tax is due on the growth until the money is eventually withdrawn. The account stays locked through childhood so it can compound, and once the child becomes an adult it simply converts into a traditional IRA in their name.

The government has put real momentum behind the launch: as of mid-2026, roughly 4 million children had been signed up and about 1 million had claimed the $1,000 starter deposit.

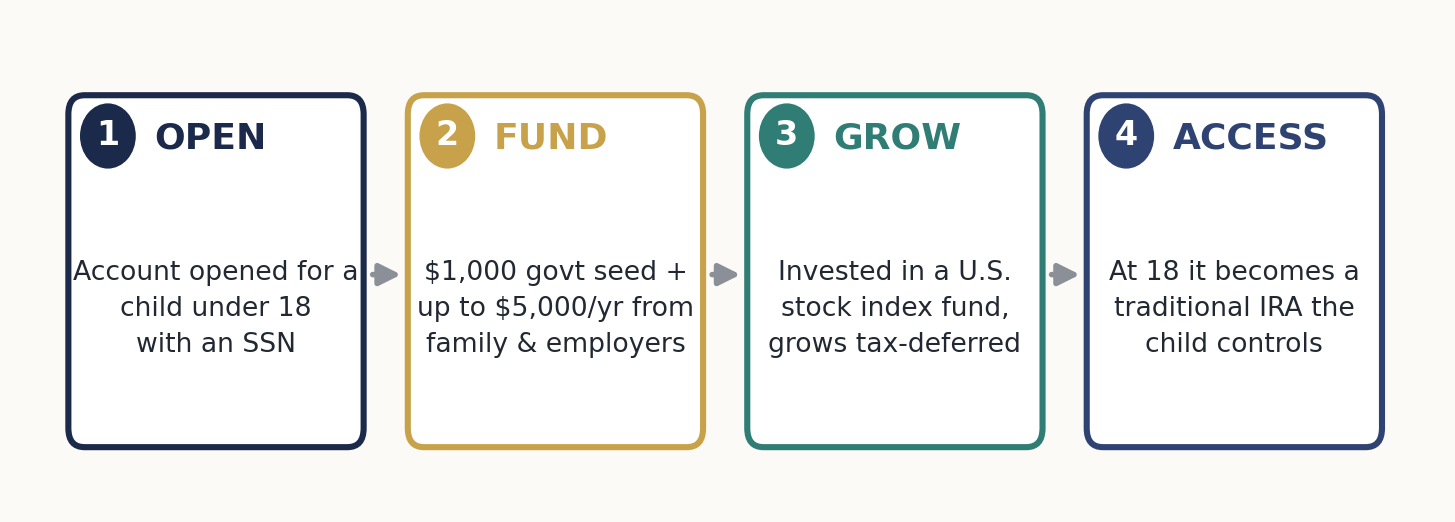

How it works, step by step

The mechanics are straightforward. An account is opened for an eligible child, it is funded from a mix of sources, the money is invested and left to grow, and the child gains access as an adult under IRA rules.

Who is eligible — and the $1,000 head start

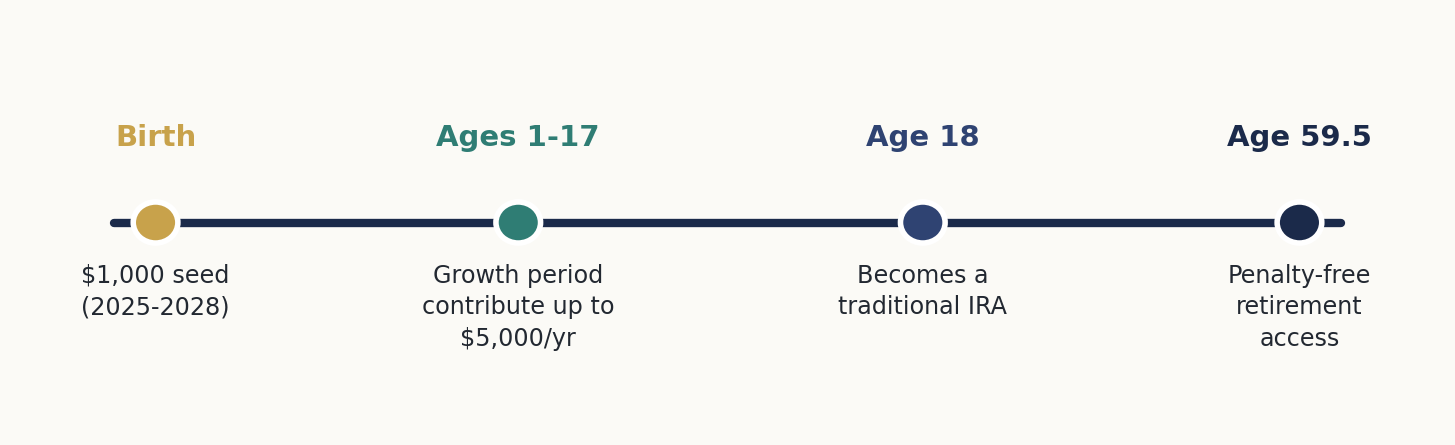

Any child under age 18 who has a Social Security number can have a Trump Account. The headline perk, though, is the one-time government seed contribution of $1,000. To qualify for that deposit, a child must be born between January 1, 2025 and December 31, 2028, be a U.S. citizen, and have a valid Social Security number. Beginning in 2028, the seed amount is indexed for inflation.

Families of children who fall outside that birth window can still open and fund an account but they simply do not receive the $1,000 government deposit.

How much can go in, and from whom

Contributions can come from parents, grandparents, other relatives, and even the child’s future employer. The rules cap the total that can be added each year: up to $5,000 per year, per child from family and other individuals (indexed for inflation in future years). Employers may contribute up to $2,500 of that $5,000 total on behalf of an employee’s child — and that amount is excluded from the family’s taxable income. The $1,000 government seed does not count against the $5,000 annual cap, and certain contributions from nonprofit or government sources are also excluded from the limit.

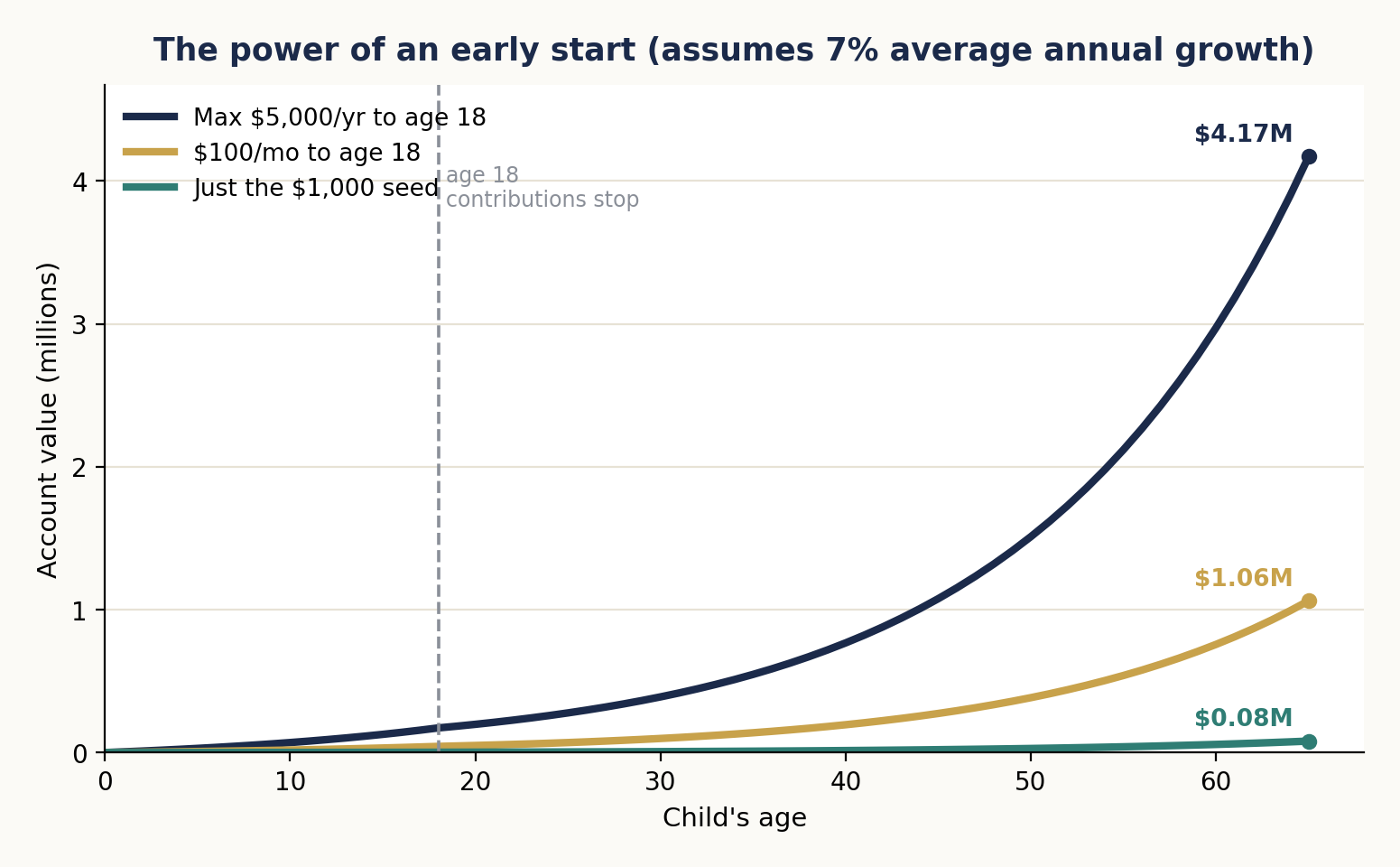

Why starting early matters so much

This is where the “dollar saved today” theme comes to life. Because the money can compound for decades, even modest early contributions can grow into striking sums. The chart above assumes a 7% average annual return — illustrative, not guaranteed — and shows three paths for a child born today: the $1,000 seed alone, never touched again, grows to roughly $81,000 by age 65. Adding $100 a month until age 18 pushes the balance to about $1.06 million by retirement. Contributing the $5,000 maximum each year until 18 could grow to roughly $4.2 million — from about $173,000 saved by the child’s 18th birthday.

The tax fine print

Trump Accounts are attractive, but they are not a Roth. It is worth understanding exactly how withdrawals are taxed. Contributions are not deductible; you fund the account with after-tax dollars. It is one of the only ways to contribute to a child’s IRA/similar vehicle while avoiding the “active income” requirement. Normally, to contribute to a traditional IRA or Roth IRA for a child under 18, they must have active income — usually done by putting them on a parent’s or family member’s payroll for work done throughout the year, an added layer of complexity for the average taxpayer.

Growth is tax-deferred, so nothing is taxed while the money stays invested. Only your out-of-pocket private contributions create a “basis” that comes back tax-free. The $1,000 government seed, employer contributions, and all investment earnings are taxed as ordinary income when withdrawn. They act effectively as non-tax-deductible traditional IRAs.

Access follows IRA rules. The account is locked during a “growth period” and generally cannot be tapped until January 1 of the year the child turns 18. At that point it becomes a traditional IRA the young adult controls. Withdrawals before age 59½ may trigger income tax plus a 10% early-withdrawal penalty, unless an exception applies, such as qualified higher-education costs, up to $10,000 for a first home, up to $5,000 for a birth or adoption, certain medical costs, or a small emergency withdrawal. At 18, the beneficiary may also convert the account to a Roth IRA.

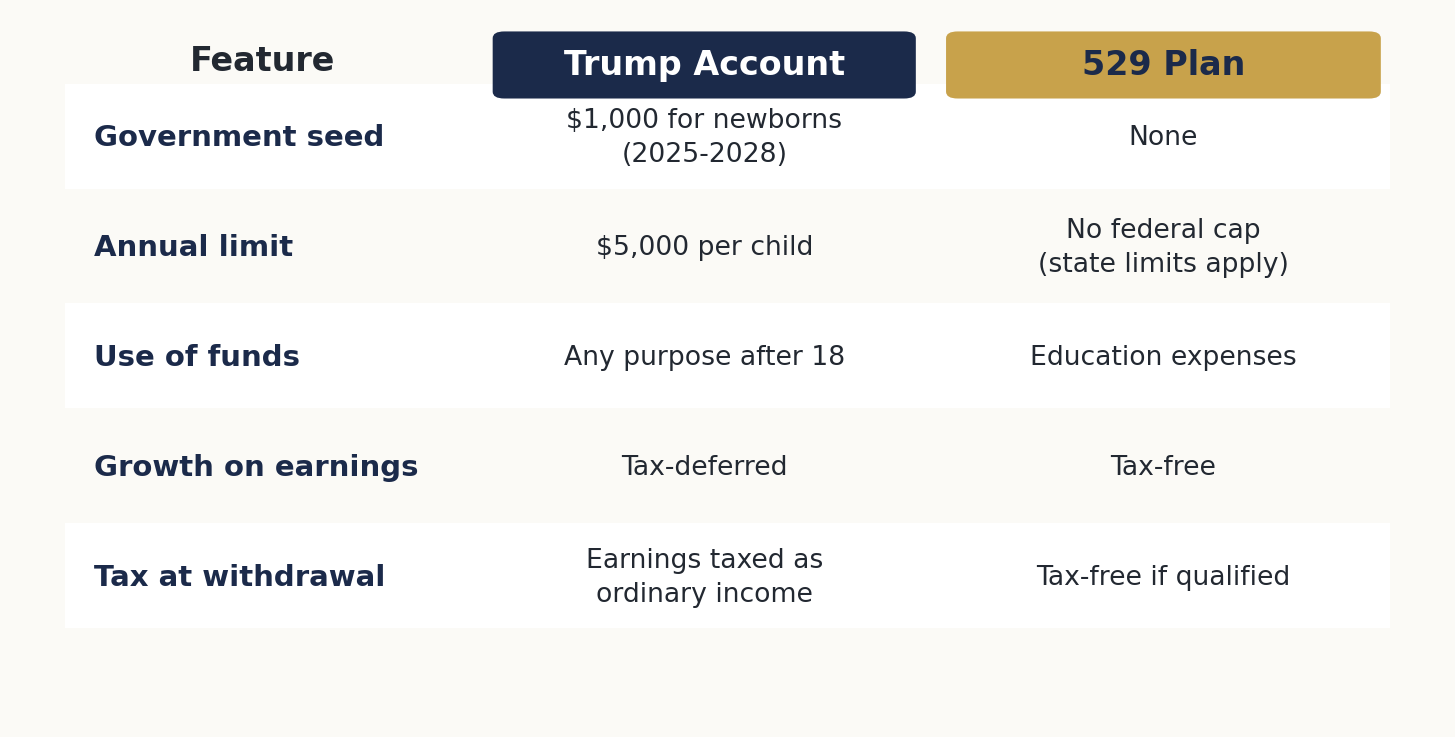

Trump Account or 529? Often, both

Many parents will ask how this stacks up against a 529 college-savings plan. They solve different problems, and they are not mutually exclusive — you can fund both for the same child. A 529 is hard to beat for education: contributions grow tax-free and come out tax-free when used for qualified school costs, with no federal annual cap. A Trump Account is more flexible — the money can be used for anything once the child is an adult — and it comes with the $1,000 government kickstart, but earnings are ultimately taxed as ordinary income.

Should you open one?

For most families with an eligible newborn, claiming the free $1,000 is close to a no-brainer. It is government money that starts compounding immediately. Beyond that, whether to contribute more depends on your broader picture: your emergency savings, retirement funding, high-interest debt, and whether a Roth IRA or 529 might serve a particular goal better. Business owners should also note the employer contribution as a potential, tax-advantaged benefit for employees with young children.